Gold captured investors’ attention with a historic rally in 2025—only to remind markets how quickly sentiment can shift. As prices surged, speculation increased, and volatility followed, the question isn’t just what happened—it’s how gold fits into portfolios from here.

In 2025, the price of gold rose 65%, its strongest year since 1979.1 In the early days of 2026, gold experienced a parabolic move, rising nearly 25% to its peak on January 29th.

On Friday, January 30th, gold snapped back, declining 12% from its peak the day before.2 The catalyst was presumably the nomination of Kevin Warsh as the next Chairman of the Federal Reserve. Mr. Warsh is viewed as more hawkish, leading some to expect a less accommodative monetary policy. This resulted in a sale of precious metals.

Going into Friday’s session, trading in precious metals had become crowded, with many short-term investors involved, some using more leveraged trades via options. The combination of crowding and leverage has led to more pronounced price movements in gold over the past few days and weeks.

In this piece, we examine the role of gold, what has driven the swift and exaggerated price movement, and how we are considering the precious metal and its investment merits.

Role of Gold

Historically, gold has served as a risk-hedging asset in portfolios. It's viewed as a safe-haven asset and often rallies when investors are fearful and seeking safety. The safe-haven role is an alternative to bonds, particularly U.S. Treasury bills, which are usually considered risk-free. When Treasury bill yields are low, the trade-off in owning gold over Treasuries is minimal. However, when Treasury bill yields are high, one must consider how much interest they are forgoing by owning gold as a flight-to-safety asset rather than Treasury bills. As such, gold tends to perform better, all else equal, when short-term interest rates are lower. In 2025, as the Federal Reserve lowered interest rates, the lower Treasury bill yields served as a tailwind for the precious metal.

A second influence on gold is its role as an alternative currency. Gold is exchangeable for currency worldwide and is even held on the balance sheets of numerous central banks. For U.S. investors, gold can serve as a hedge against the U.S. Dollar, where a notable depreciation should, all else equal, lead to a rise in gold's price. In 2025, a decline in the U.S. Dollar served as a further tailwind to gold prices, helping to fuel its outsized gain.

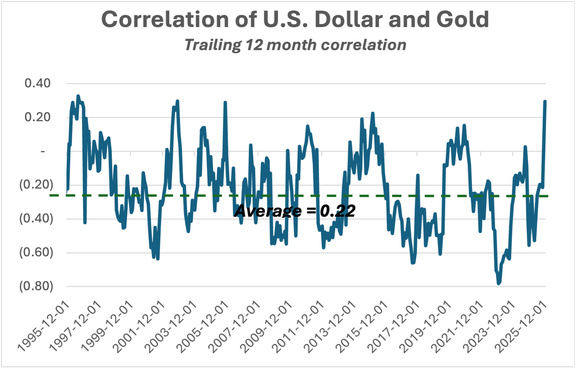

The chart below highlights the correlation between the price of gold and the value of the U.S. Dollar. Over the past 31 years, the correlation has averaged -0.22, meaning the price of gold has typically moved in the opposite direction of the dollar.

The U.S. Dollar is proxied by the Bank of International Settlements Real Broad Effective Exchange Rate for the United States.

Source: Composition Wealth, Bank of International Settlements, St. Louis Federal Reserve FRED database, LBMA. January 1995 - December 2025

Gold’s role as a diversifying asset has become more notable in recent years. Following the Federal Reserve’s move to raise interest rates beginning in 2022, the returns of stocks and bonds have become much more correlated than they had been for much of this century. As a result, some investors have begun to view gold as an additional portfolio diversifier.

Recent Influences on the Price of Gold

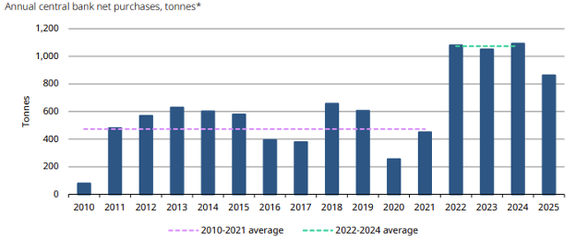

Central bank purchases have been a persistent trend supporting gold prices. In fact, buying among central banks has been elevated in each of the past four years. However, in 2025, purchases fell by 21% from the previous year.3 The chart below highlights annual central bank purchases, which have been elevated in recent years, with a step down occurring in 2025.

Source: World Gold Council, Metals Focus, Refinitiv, GFMS. As of December 31, 2025

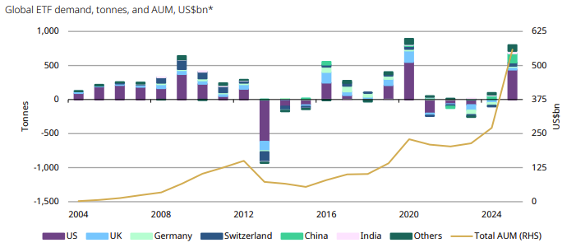

The replacement of demand for gold from central banks was replaced by interest from individual investors, which manifested in a significant way in the back half of 2025. In fact, inflows into gold exchange-traded funds (ETFs) were positive in each of the last six quarters of the year. Of the gold ETF demand, 62% came from U.S. investors.4 The aggregate demand, however, was widespread, with insatiable demand emerging from Asia as well. Of note is India, where ETF inflows totaled $2.9 billion in 2025, nearly equal to cumulative gold ETF inflows from Indian investors during 2020-2024.4 In China, demand also surged as investors sought alternative investment options following declines in real estate and equity prices.

As the chart below shows, global ETF demand increased sharply in 2025 after declining in each of the previous four years. Inflows into gold ETFs marked the most significant demand for gold investments among individual investors since 2020.

Source: World Gold Council, Bloomberg, Company Filings, ICE Benchmark Administration. As of December 31, 2025

An offsetting driver of gold demand was a drop in jewelry sales. Not a shock given the significant price rise, with global demand for gold jewelry falling 18% during 2025.2

Putting these pieces together, the demand for gold in aggregate increased by 8% in 2025. With global demand now at 5,000 tons, it exactly mirrors global supply, which also sits at 5,000 tons. Therefore, the evolving behaviors of central banks, individual investors, and jewelry owners have brought supply and demand into equilibrium.

This even balance did not lead to an easy start to 2026, with the 25% surge throughout most of January marking the fastest move in gold prices this century.5 A contributor to this swift movement was a record wave of call option purchases on gold securities5 that began late in 2025 and continued throughout January.

Gold’s Role in Portfolios

Historically, gold has delivered an average return of 4%, roughly one-third that of stocks, with greater volatility.6 Gold's benefit to a portfolio, however, comes from the diversification it provides. The price of gold tends to move independently from that of stocks. In fact, over time, the two assets have correlated at 0.03, or effectively no statistical relationship in their movements.

As we look at how gold might fit in an investor’s portfolio today, we have to consider it in the context of the current climate and the factors driving its returns. The notion that gold can serve as a diversifying asset and serve a role in portfolios should the U.S. dollar experience further depreciation is a valid argument. This notion, however, must be considered alongside alternative approaches such as holding more bonds, which offer a level of safety relative to equities, and owning international assets, which can serve as a hedge against dollar depreciation. Given current price levels, we see the combination of bonds and international holdings as more compelling at this time.

The reason for this view is threefold:

- We believe Federal Reserve interest rate cuts are largely complete, with possibly only one or two cuts remaining. Therefore, the tailwind of lower short-term rates is likely limited.

- As we look ahead, we foresee some resolution to drivers of fear around the debasement of the dollar. Friday’s nomination of Kevin Warsh as the next Fed Chair should provide some reassurance about Fed independence. A looming Supreme Court decision on the use of IEEPA to impose tariffs should provide some resolution on the scope of presidential powers to impose tariffs. Regardless of how these matters play out, resolving the overarching uncertainty could reduce investor angst and the need for a gold hedge.

- We see excessive speculation in gold. Friday’s sell-off likely removed some speculative investors and reduced exposure among those gaining exposure through more leveraged means. We’ll see how trading goes in the days and weeks to come and whether it washes out the speculative behavior in the precious metal market.

CONCLUSION

Gold has swiftly become a more desirable asset following its accelerated rise in 2025 and strong start to 2026. As we do with all investments, our assessment considers the potential return, the range of risks, and its role in a portfolio. Gold can serve a purpose in some investors' portfolios; however, today, the risk potential, and in particular the drawdown risk after a speculative-driven price uptick, warrants caution. We project gold prices will remain volatile throughout 2026, at levels above historic norms. As geopolitical conditions normalize, we expect gold to return to its role as a diversifying, safe-haven asset. However, this will likely take time to take hold.

Source: State Street Investment Management. Based on the LBMA Gold Price Index.

- Source: Bloomberg. As of 4:00 pm on January 30, 2026.

- Source: World Gold Council, Global Demand Trends Q4 and Full Year 2025. January 29, 2025

- Source: State Street Investment Management, Gold 2026 Outlook. As of December 5, 2025.

- Source: Bloomberg, Maco Man. January 29, 2025. Cameron Crise.

- Source: Zephyr Style Advisor: Gold referenced by the LMBA Gold Price Index. Stocks referenced by the S&P 500. Analysis period March 1980 – December 2025.

Disclosures: Composition Wealth LLC (“Composition”) is a registered investment advisor. Advisory services are only offered to clients or prospective clients where Composition and its representatives are properly licensed or exempt from licensure. The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward‐looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur. The information is illustrative, provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. Asset Allocation may be used in an effort to manage risk and enhance returns. It does not, however, guarantee a profit or protect against loss. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. All investments include a risk of loss that clients should be prepared to bear. The principal risks of Composition’s strategies are disclosed in the publicly available Form ADV Part 2A. Past performance shown is not indicative of future results, which could differ substantially.